Cannabis: Ponzi & Zombie

Are you even paying attention?

PONZIS & ZOMBIES ABOUND

The state led growth story in the cannabis industry is a funny one.

State growth is a proxy for revenue growth.

Revenue growth is a proxy for EBITDA growth.

EBITDA growth is a proxy for cash flow.

People are using a proxy for a proxy for a proxy that doesn’t even translate well due to usury interest rates and astronomical taxes levied against the companies. Just as strange is the fact that most people are ok with this.

Many of these MSOs need constant state expansion to maintain the appearance of growth & success. These company's growth strategies heavily rely on continuously opening new markets (states) because they’ve failed to demonstrate sustainable profitability in existing markets.

They need new markets to pay for their now unprofitable older markets. The reason being is that their profits have atrophied due to the inevitability of prices normalizing. These MSOs require abnormal prices to maintain profitability. And those abnormal profits disappear after a year or two.

Might you notice the parallels between these MSOs and a Ponzi scheme? The requirement of new investments to generate cash flow to pay off old investments due to not actually being self-sustaining. Now in reality, they’re not a Ponzi scheme but the state led growth story is very Ponzi-esque. More accurately, many of these companies are zombie companies. They don’t organically generate enough cash flow to sustain their business and thus need to externally raise more money.

Many of these companies need state churn. It’s crucial for their narrative. And when that isn’t enough, they need to entertain the idea of potential government catalysts to keep the narrative intact. Each new “next” thing is the savior of the industry. In reality, it’s just a temporary means to prop up the narrative but not to improve or address the rot in the company's business practices. Pretty fictional stories meant to conceal the truth sound familiar to what Mr. Ponzi did too.

It’s a chronic churn of shifting the goal post. Each new state will be what will help the industry. But let me ask you this, how many states have now legalized? And how much better off are these companies? To me it would seem that each new state that comes online makes matters worse not better. Of course, I’m speaking in generalities, but it does hold true in large part.

The crazy part is that this is within the confines of what amounts to a pseudo-oligopoly due to limited licenses and interstate commerce not being allowed.

Each boom state becomes an eventual bust state. It’s not just because of the state but because of these companies' business strategy.

It’s one of simple game theory. As I outlined in this article. The below image is in regard to shipping companies, but it just as well applies to cannabis companies.

This is not a flaw but a feature. Their strategy was to expand as rapidly and if need be, as unprofitably as possible. The unprofitable part is a foreseeable product. Like I said, not a fluke or flaw but part of the overarching strategy.

This is nothing new and these results should have been expected.

Simply put, normalized prices are a death sentence.

I’ve outlined some of these dynamics in the Arc of Development of New Industry section of an article I’ve written here:

“A flood of cheap capital pours into a new sector or industry. This leads to over-investment, which leads to over-expansion, over-production and over-capacity. At the onset, demand outweighs supply. This leads to the first movers making profits. The analysts normalize those profits for future projections. But the profits will soon disappear. Because as often is the case the market is heavily fragmented. In the case of cannabis, this leads to each player saying something along the lines of, “Look how much money we’re making on a 10,000 square foot grow just imagine if we expanded to 100,000 sq. ft.” The lead time to build gives a false impression at sustainable profits but inevitably a deluge of supply comes online. Such projects are expensive, so they’re interested in undercutting competition to recoup their capital. This flood of supply overwhelms demand, profits get competed away, margins compress from positive territory to negative territory, they take on debt to stay afloat and inevitably bankruptcy and consolidation occurs in the industry.”

Like I said, this shouldn’t come as a surprise to anyone. The concerning part is that the vast majority of people still don’t know what’s happened over the last half decade. At best they have a low resolution and ill-defined conceptual idea along the lines of, “They’ve been working out the kinks and not everything has gone as planned and it’s the government's fault.”

THE GAME HAS CHANGED

People aren’t paying attention…The game has changed.

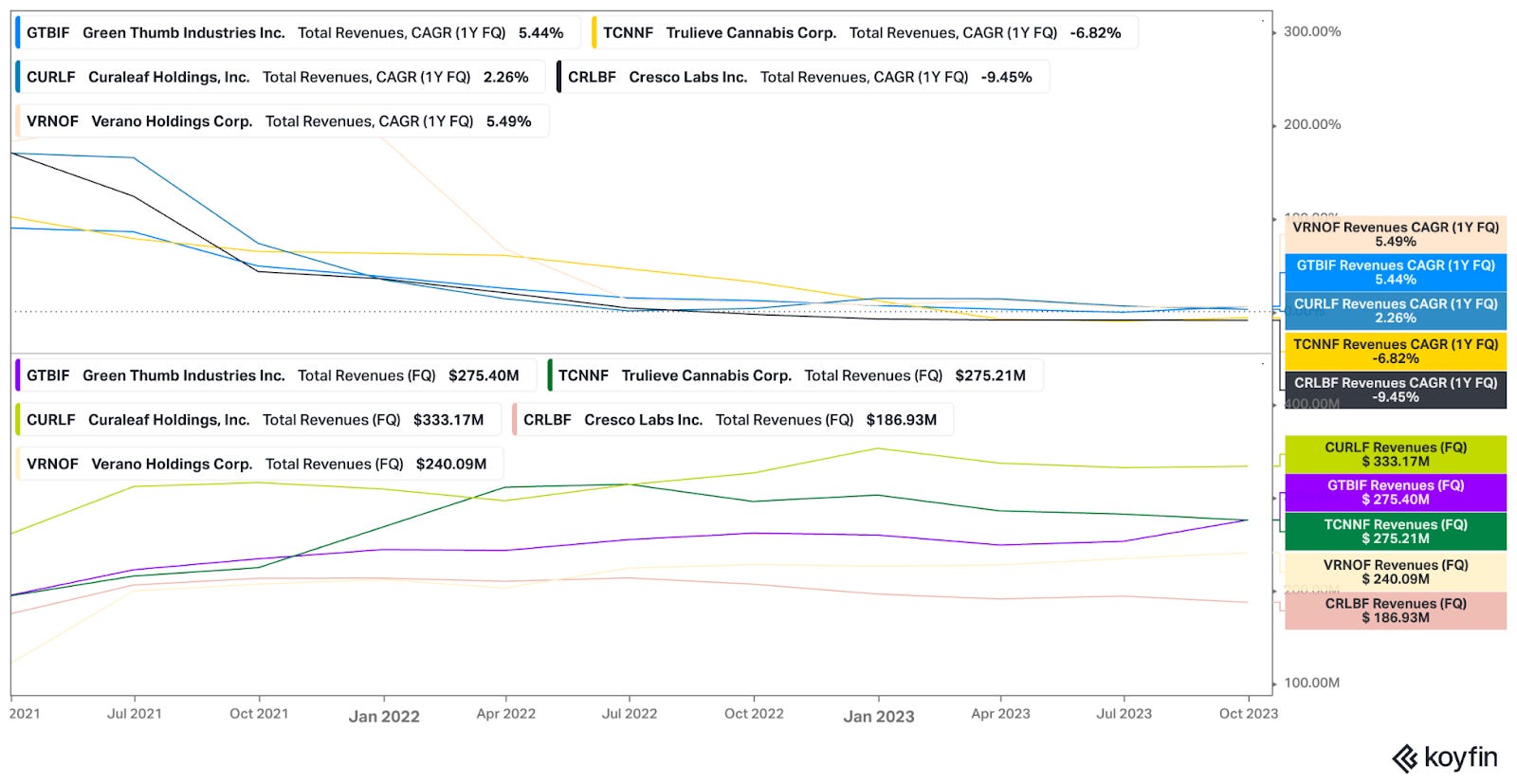

The hype isn’t what it used to be and the rate of change of growth has deteriorated, and revenues are stalling.

In an intellectually dishonest fashion, I’d expect many to start moving their goal post from EBITDA to gross margin to revenue and more recently debt paydown. They might go from talking about EBITDA margins to EBITDA in terms of total dollars in order to ignore collapsing margins. So on and so on. It’s classic thesis creep brought to you by ideologues who wish to only use data that supports their beliefs.

Growth in the form of capex spend was the distraction mechanism used to justify their stock multiples.

Let's look at this chart.

Are these companies sufficiently built out and started turning profitable?

Were these companies over leveraged and needing to slow growth to plug the hole in their balance sheet?

How does this reduction in future growth via capex spend bode for their future growth?

Remember, state growth demonstrated via capex spend is a necessity (other than federal legislation) to keep the Ponzi-esque structure of business going. New states plug the hole and distract from the older states that are wreaking havoc. Their opaque disclosure for same store sales has been given a pass because they were showing top line growth. When times are good people don’t ask questions.

Each new state is making a relatively smaller contribution to the overall picture due to their increasing footprint. It’s a simple problem of base effects.

A new state will not make up for the malfeasance that’s occurred in a dozen states.

People will use the above images as to why federal legalization needs to happen so that these companies can grow. But they’ve been growing. It also ignores how many of them have been terrible stewards of capital for the shareholders. It’s been great for the debt, preferred equity and C-suites constituents. What makes you think that they’ll start acting intelligently now? Much of the evidence is to the contrary. Why wouldn’t it be another bum rush of poor capital allocation in a land grab fashion and a redux of the early days?

I hate to break the news to you, but these Tier 1 MSOs aren’t growth stocks. They WERE growth stocks. But as I’ve outlined to you, the game has changed. Their best days of super-growth are behind them.

Nearly 80% of states have legal medical use and 50% of states have legal recreational use. This means that they’ve captured roughly 60% of the market based upon states. According to Statista half of citizens/consumers live in states with legal use.

Remember the Ponzi-esque strategy I outlined earlier? These companies need new states and new consumers to stay afloat. Well, it’s getting tougher and tougher as they run out. They’re halfway through and have yet to be proven to be profitable.

Guess it’s a good thing that Germany has legalized, that’ll keep the narrative going.

These companies' modest or nonexistent profits in mature or maturing markets are weighing down the short yet profitable gains in new markets. Roughly 80% of states have medical and 50% are recreational. Their best days are behind them in regard to being a state led growth story. Yet people in large part haven’t clued in. They’re engrained and emboldened through their desensitized following of old narratives back when states mattered more.

An irony of this is that these speculators are telling the government to catch up to the times and yet their investing strategy has yet to catch up to the times.

The problem is that the game has changed. They’ve gotten to the point of diminishing returns. A new state doesn’t have the same impact that it used to. Going from 1 state to 2 states is a 100% growth rate. Going from 12 states to 13 states is 9% growth. And that additional growth isn’t enough to stop the hemorrhaging that’s occurring in the maturing markets that they have a footprint in.

TIER 1 MSOs STRATEGY

They bum rush into a state, capture the high profits and high margins and then move on to the next state. They’re taking the cream off the top. The problem is that they still own and are paying for the lingering residual business in the aftermath and fallout. It’s not like they can pack up and go to the next state with their PP&E. They have to build out and do it again, state after state after state after state after state after state after state.

The residual operations bleed out and hemorrhage cash. And that necessitates the importance of the next state. But they compound their baggage of left over states and the new state can’t offset and compensate all their other failed states. They’ll pull out of some but keep most. They’re playing the limited license game via a temporary supply/demand imbalance. They’re in it for the quick grab. The problem is that they’re stuck because they put a proverbial baby in the state and now they have to tend to it and this metaphorical baby isn’t paying for itself.

It’s a hit it and quit it mentality. It’s a smash and grab. A dine and dash. Yet they can’t “quit it” or “dash”.

This theme I’m describing to you has played out enough times that the management teams should know not to go into a state if they can’t make profits above the levelized and normalized cost of production. This is basic commodity economics 101. But they keep going into new states. WTF!

The average stock speculator only adds fuel to the fire. It’s as though they don’t know how to differentiate between mid-cycle earnings and peak-cycle earnings.

I had a tweet about how it would be more accretive for these companies to invest in T-bills than their own business because their ROC is less than T-bills. This is an implicit statement and condemnation that these companies are value destructive. Shareholders can't deposit gross margins into their bank accounts. But the inept observer prefers a vegetative state, unplugged from reality, in order to maintain their delusion and not disrupt their Disney-esque fantasy. It’s Cope & Fallacy.

A simple rebuttal would be for them to show line items of their performance metrics in individual states. Such as how their comparable sales fair while using the same store data. But they don’t. Why? They’d prefer to obfuscate because it wouldn’t be beneficial or flattering to do so and it isn’t required or expected of them. This is the opaque market that they’re in…for now. The devil is in the details. They don’t want you to separate the wheat from the chaff because they don’t want you to see their rotten kernels.

I expect at some point in the future that they will provide higher resolution data. But that day will come when institutional traders (the adults) start participating in these names. The funny thing is how so many retail investors say that for these names to rocket they need more volume and attention from professional money. Yet again, I think the opposite. Professional money will see these companies for the garbage that they largely are and will want no part. Retail can’t understand that because retail doesn’t understand arithmetic. Plus, it clashes with their ideology.

These companies have flatlined and are getting desperate. Of course, necessity is the mother of invention so perhaps they’ll make some profits by righting the ship and tightening up their finances. But remember they move as a group. They need others just as desperate so they can tacitly collude. They need a price leader. And may I remind you, it’s not as though their revenues have flat lined but they’re printing profits. They’ve flatlined revenue and are unprofitable. Ouch!

DUMB MONEY

I don’t generally care for that pejorative term when referring to retail investors. But the shoe does fit in this case.

The best and simplest explanation of what’s happening is twofold. They’re political hobbyists and are engaging in ideological investing. There’s a lot to unwrap there in those placeholder words.

I’ve touched upon this ideological investing numerous times, here are a couple of instances where it was the predominant theme. Here and Here.

I’ve not published an article on political hobby-ism, although one is in the works. Simply put, a political hobbyist is someone who is unbeknownst to themselves engaged in politics for enjoyment, entertainment, emotionality and as a way to bond with peers. However, their engagement is shallow and is primarily one of consuming content without ever actually understanding or reflecting on it. Features of political hobby-ism are manufacturing outrage and indignation, pontificating, mental masturbation, cheap thrills and infotainment.

This is why many investors think feel that legal measures or institutional traders getting involved is a positive. To them it’s a foregone conclusion.

I don’t believe in forgone conclusions where people go from thesis to conclusion. I believe in the antithesis and synthesis components of the decision-making process that’s part of the dialectic reasoning process. I outlined that idea here under the segment Thesis, Antithesis, Synthesis.

Yet these bag holders have trauma bonded and seemingly their ethos is similar to Stockholm syndrome. They have a ready impulse in excusing the captors of their capital. The cognitive dissonance is strong in them. Unaware that they’ve been swindled into believing the state led growth Ponzi scheme with the subtext of a legislative catalyst. And as such, they’ve developed a schema to explain it away. Cope & fallacy for the win.

These people are sick, twisted and deranged. They take being a bag holder as a badge of honor and treat it as a point of pride. So why wouldn’t they excuse the sin of their management teams when they themselves were poor allocators of capital. I touched upon this psychological phenomenon known as “projection” in an article I’ve written, it’s under the Word of Caution segment.

It would be wise of you to recognize that you’re doing it. Because it means you’re lowering your standards and tolerance of what is and isn’t acceptable. This implies you have a low hurdle rate for an investment which increases the probability of you losing money. It’s kind of important not to lose money.

Most recently I heard a guy on a podcast say that he doesn’t factor in opportunity cost into his cannabis investing decisions. WTF!

The degree of pathology I see that’s grounded in ill-conceived misnomers in the form of misguided conventional wisdom is alarming. They’re sentimentality focused and valuation agnostic. Quit simply because they don’t know how to value the business. Infotainment with a bent-on agitprop is where they’re focused. Swooning over headline porn or anything that confirms their narrative. They’re preoccupied with force fitting their narratives and agendas into conversations and then readily jumping to allegedly forgone conclusions.

Their arguments are superficial rhetorical smoke in mirrors spoken in a specious fashion. Cope & fallacy is their kabuki theater and Potemkin village. They’re concerned with pontificating their ideas and mentally masturbating then they are at gaining a cursory insight into the markets.

They’re always chasing the next shiny object, soon to forget the old shiny objects that their companies are selling off at a massive loss or taking impairments on ($225M impairment of Curaleaf). And if they do remember, they congratulate the management team for doing so because they’re right sizing. LOL

Buying companies that need government catalysts is playing the wrong game. Buying companies that are their own catalyst and internally managed well is the correct game.

THE WRONG LEVEL OF ANALYSIS

I’ve come to the conclusion that most people most of the time view things on the wrong level of analysis. A large part of that is that people direct the framing of a conversation in a way that’s flattering and beneficial towards them, not necessarily in the direction of reality.

For example, in one of my articles on cannabis I noted how people were justifying the earnings multiple of a stock by comparing it to even more expensive stocks. They measured it relatively instead of absolutely. Put differently, they essentially said that a stock was a buy because it was less expensive than a more expensive stock. Umm…. what?!

With that said, anytime anyone is viewing something on a certain level of analysis I presume that it’s the wrong level of analysis. In this case, the amount of attention superficially dedicated to the federal level hints to me that this is probably the wrong level of analysis to be a successful investor in this space.

I don’t care if cannabis becomes federally legal on every possible level come tomorrow. I’m not buying cannabis stocks at a 50x P/S ratio let alone 10x P/S. And yet, market pundits were trying to justify doing that very thing a few years back. That’s really worth thinking about. And they used the same growth story to validate it. The same growth story that they’re still using to this day.

So, what’s with this obsessive fixation and compulsion to focus on the federal litigation? It’s a hot button issue. Also, in any short-term time period (which is most people's investing horizon) it’s a low probability high magnitude occurrence. That’s the level of analysis they’re viewing it on. And what did I tell you about people's level of analysis?

And if you want to get crazy, you could view the companies on such measurements as Return on Capital or their Debt Service Coverage Ratio.

Remember, half a decade has been laden with people focusing on the meta and forgoing the micro. It’s exactly that which allowed people to ignore buying a company at 20x sales, 50x sales and earlier on 100’s of times sales. It’s because they were focused on the wrong details. The more crucial and pertinent details that would determine their returns (statistically and historically speaking). Yet again, it isn’t that federal litigation doesn’t matter, that’s the wrong framing and level of analysis, it’s that there’s other things that matter too.

You should care about the bullish catalysts that you can evaluate, build confidence on and structure a portfolio around with confidence.

I own a Master Plan Community developer in Florida, the St. Joe company. And then people want to know how the PMI falling in Europe might impact my thesis. WTF? Why do so many people think that they have the capacity to view matters in such a macro and obtuse fashion and to think that they’ll then know how that will trickle down to such micro matter? Yet again, it’s the wrong level of analysis. The problem is that these hubristic fools will come to a conclusion, it just won’t be the profitable one.

A NEW STATE IS COMING ONLINE!

There’s a new state that has recreational use on the ballot!

There’s a new state that legalized recreational use!

Who cares?

Which isn’t to say that it doesn’t matter per se but how much does it matter? And HOW does it matter? To what extent does it matter? And perhaps if you’re so daring what else might matter? Since 2018 the number of states allowing recreational use has gone up 100’s of percent. Yet the stocks aren’t triples. For the most part the stocks have crashed 50% plus and that’s being generous. You would think that this massive divergence might make a person ask some questions. Such as, what role does a new state coming online have in my pot stock investment?

Yet again, this isn’t to say that a new state coming online doesn’t matter. It most certainly does. We’re now at the point of nearly half the states legalizing recreational use. That’s a big deal optically. And since people behave based upon optics it can most certainly influence behavior. What behavior? How about the politicians getting their act together?

We’re to the point of nearly half the states legalizing recreational use. But this creates hazards. For instance, you run the risk of not having enough bandwidth to pay attention to what’s happening in all the other states outside of headline big news. The companies don’t make it any easier on you because they refuse to break down the numbers by market. I can assure you that most people struggle to listen to a conference call let alone pay attention to all the moving parts which are independent states. How many people are paying attention to flower prices in each of the respective states?

Someone will talk to you for 15 minutes about all the exciting news about a new state coming online but they can’t tell you what’s going on in the other states that the company is operating in. Like I said earlier, they just chase one shiny thing after the next.

People might point out that cash flow is increasing but fail to mention that’s the consequence of accounts payable piling up and taxes not being paid. Like I said, people view things on the wrong level of analysis. Flattering information is regurgitated and unflattering information is swept under the rug. You’ll come to find out too that these people don’t do their own research. Which means that whatever they say and think is from the demigods they worship, and those demigods have the perverse incentive to only say flattering things. Remember this next time when someone only has positive things to say. It’s a symptom of a non-playable character who doesn’t think for themselves and is barely sentient. Their speech has been constrained and censored for them due to them primarily being a regurgitating rote promoter. And they’re clueless about this.

PUTTING THE CART AHEAD OF THE HORSE & HOW THE TAIL WAGS THE DOG

It isn’t that legislation isn’t important, it’s that other things are important too.

It isn’t that one shouldn’t entertain these ideas, factor in the considerations, come up with a spectrum of probable and possible outcomes both imminent and inevitable and weigh counterfactuals. That’s all important and crucial to developing contingency plans. Foresight is forewarned and forewarned is forearmed. But I get the impression that all this top-down pontification is being done at the cost of doing prudent bottom-up research.

All of us only have so much time, energy, focus, cognitive capacity and processing power. Even if you got all the answers to all the questions you have around the federal matters it still won’t tell you what to buy.

Or…you could look at companies from a bottom-up approach, assume current conditions stay the same or improve and model what that would look like. One of these strategies gets you invested, and one doesn’t. And I can’t help but think that’s not an accident. People want to run their mouths with minimal to no skin in the game versus putting in actual work and disciplining themselves. It’s no wonder the vast majority of people have a behavioral preference for the former over the latter.

The Serenity prayer is needed in this space.

When all that seemingly matters is legislative reform all the companies in this sector get a free pass, right? Their sins are absolved. But I think that’s a horrible way of looking at things. Very few are cognizant of the fact that some operators have done well while others have done terribly. Oh sure, they’ll recognize it on an intellectual and philosophical level, but they won’t deploy and manifest that wisdom in their behavior.

Here’s a fun question to ask these people. If everything you ever could dream of happened tomorrow, how much would you pay for these companies? What is it worth??? 100% 's of percent above where it’s at is what I’ve heard from some. So, if it opened up 50% on the day with news like that, you’d be a buyer? After all, you’d have 100’s of percent upside?

My guess is that they wouldn’t. That’s really worth thinking about.

IN SUMMARY OF THE ABOVE

The idea of an “embedded growth” story around the potential of new states is a fool's errand and an evergreen pipe dream. So, all one needs to do is see how they’ve fared in other states. The reason they’re not profitable is because of their failings in other states. It would go to the reason that unless they’ve done something radically different that trend will continue. They’re awkwardly fumbling forward, selling pipe dreams which entices people to pour money into them. It’s that external cash flow that keeps them propped up, not internally generated organic cash flow. And that is what makes them a zombie company.

New state expansion buys them time. The state led growth story is a Ponzi structure. You need new states to pay off the sins of the old state. They’re not trying to pay the piper. Both because it’s outside of their strategy but also because they literally can’t. Or that’s all they can do is pay the piper (and themselves of course), after which there’s no money left for shareholders.

This is a conflict-of-interest dilemma I’m speaking to you about. A principal-agent problem. It’s control fraud (of the legal kind). A so-called bust out. They’re largely lifestyle companies.

The implication is that these companies can only do well when times are good. And since good times taper off, then so will their ability to do well. Which leaves what? Them doing poorly. And it should be no coincidence that you will be poor by investing in companies doing poorly. Yet the secured debt holders, preferred equity and C-suites do quite well.

There’s more than one way to express a view. And I’d say thus far the institutionally managed money, family offices and accredited investors have made smart moves by investing in those vehicles rather than the public stock.

It’s clear that as prices normalize due to a balanced market their margins get squeezed. Since they’ve not taken the time to be profitable in a normalized priced market (everything is eventually going to go the way of California & Canada) they’re profitless companies in perpetuity. Legislative reform will give them a boost but like any good hedonic treadmill, that too will normalize. I suspect it’s a stair step function to break-even NOT necessarily profitability. I outlined in my Game Theory article concerns I have in regard to this “blue sky” optimism.

I want operators who’ve demonstrated core competence in capital allocation and concerns towards operations. I want them to have the wherewithal and faculties via their creative productive capacity to identify problems, generate ideas and formulate solutions. That’s a rare trait to find due to the mass cranial-rectal inversion that many management teams suffer from.

We must look past Capex as a proxy for growth and stop treating growth as though it’s always a good thing in a decontextualized matter. As though growth is a means in and of itself. Many seem to forget it’s a means to an end. When you bring up many managers' records, people look past it.

The best I can tell is it's sort of like this:

It’s a “we need to spend just to tread water and maintain relevance, so we don’t get usurped and lose our spot, place, status and claim in the pseudo-oligopoly hierarchies that have been created from regulatory capture.”

This would explain why I’ve been talked down to when I bring up return on capital. People care about the deployment of capital but not its return. It all gets swept under the rug with thought terminating cliches formulated in an ostensible fashion such as, “the cannabis industry is in its infancy stage, and they need to grow.”

But yet again, that presupposes that needing to grow in an industry in its infancy stage requires you to be profitless. That’s the idea that people have in their heads. They’ve become conditioned, habituated, trained to act that way. This has been reinforced in them by their culture and peers and has led them to be desensitized to meaningful metrics of performance. As a matter of fact, it’s nearly become taboo to speak of profitability metrics.

These people have this idea that if a company keeps growing that it’ll eventually end good. They have no evidence for this but that won’t stop them with some anecdotal exception to the rule to support their case.

In large part, large MSOs have poor (literally & figuratively) business models.

The large players always get the most fanfare, that’s just how it works. MSOs would be international conglomerates if each state was thought of as a country. This is why they don’t have economies of scale; the unit economics just don’t work. If anything, they have diseconomies of scale.

Have they gotten better and leaner, pushing out better quality products at lower costs? Have they revamped their more mature markets? Each state is siloed and cut off from the others. Once interstate travel opens up then you’ll have a bunch of abandoned assets and accompanying write-downs. Why grow in Maine in a costly warehouse when you can buy a plot of land in California and grow outside or in a greenhouse and ship it to Maine?

The state led growth story is one of operators desperate for flesh blood (cash flows). When each state was once a boom and is now a bust you see why external factors become more relevant because these companies are more necessitous. These companies are hammers and everything looks like a nail. Unprofitable operators blame the markets instead of themselves. It’s classic blame shifting and D.A.R.V.O. It’s propaganda.

It’s under this framework that you come to understand people's focus on the state led growth story and political catalysts. It’s an admission and recognition that these companies are dead in the water and a lost cause without external support.

This neurotic, obsessive fixation in regard to the state led growth story and political catalysts is for a reason. These companies can no longer rely on state expansion in and of itself. These companies now need external catalysts to compensate for their internal blunders. This is where legislative reform becomes important. They need larger and larger catalysts to keep them treading water. They need to show short term growth to maintain the rhetorical smokescreen of being a growth company. This is why you see hype around Germany or Poland. It’s not because it’ll make a meaningful difference to their financials but because it’s crucial in maintaining a narrative of so-called growth.

A problem with this obsessive, pathological and neurotic fixation with litigation and reform is it results in the byproduct of excusing unprofitability. This attitude normalizes unprofitability by excusing it due to externalities. It shifts the locus of control that management teams have and places it on some external, existential malevolent predator (the government).

I don’t care too much about the DEA, HHS, blah blah blah blah blah. I’m not going to bother myself or waste my time with such an existential looming situation so I can get all hot and bothered. Now does that mean I haven’t considered the implications of it? No. What it does mean is for all intents and purposes I could care less about the *NEWEST DEVELOPMENT*.

After 5 years of crying wolf, you’d think more would share in this attitude. But nope. When that’s the catalyst you’re hoping for, you're already screwing up.

I look at 280E or any such matter as an afterthought, a bonus, an optionality play. Not the damn focus of my thesis. Not as crutch that self-imposed, unforced erroring, desperately handicapped companies need to stay solvent.

I wouldn’t be surprised if they told their shareholders some nonsense like this.

DIFFERENCE IN BELIEFS

The difference in axiomatic beliefs is why this can’t be resolved. One believes slow and steady (rabbit and hair) wins the race. The other believes the insatiable appetite and radical unhealthy growth wins the race. They think that slow and steady gets left behind and loses competitive advantage. But they’ve not learned the moral of the story and its lessons. Yes, optically you do get left behind. But what are you betting on? Are you betting on who’s leading the majority of the race or who’ll cross the finish line first or at all? The problem is people conflate those two to mean the same. When the incentive structure for those running the race (management) is a compensation package predicated on EBITDA and Revenue then perverse incentives will occur.

There are two different games being played.

Style #1: take advantage of short term (perhaps a couple of years) price and accompanying margins. Also establish a foothold via a first mover advantage. Once prices normalize, they’ll be unprofitable, but they get to show growth for a couple of years. At which point hopefully they can do it all over again in another state. But this leaves many corpses behind and zombie operations. Immediate gratification with strong initial profitable impulse.

Style #2: Coming up the rear, they’re slow and steady. They’ll often get there later and won’t be able to profit off of the initial supply demand imbalance. The established foothold of first movers will deteriorate over time as more profitable players take market share and usurp them. However, this sort of player will be profitable because they’ve taken the time to dial in their skills.

These players have stayed within their means for years, honing their skills and dialing it in. They’re capable and competent in providing quality and a price less than their competitors while remaining profitable. They’ve sharpened themselves and now they have an edge. They’re now ready to expand and that’s exactly what's happening.

Why are the vast majority of cannabis companies unprofitable?

Well…why?

If you’re like most people, you’ll blame the government.

Let me ask you this then. How are there profitable cannabis companies?

Remember that variable that you cited as a reason for why most cannabis companies aren’t profitable (the government)? Well, if you could be bothered to keep constant your comparisons and control for variables, you’d realize that the profitable cannabis companies are also affected by the same government.

Now you might say, “But if it was federally legalized then the companies could be profitable.” But that argument presupposes that federal legalization would make the vast majority of cannabis companies profitable. Which doesn’t seem obvious to me.

And why do I have to tell you that by profitable I meant positive net income. It’s as though you’ve become pathologized by constant gaslighting that you’ve come to believe that EBITDA is profit.

Strange, don’t you think? Do you manage your own finances based on EBITDA? Why not? Who cares about take-home-pay and having the capacity to pay bills? After all, aren’t you a growth story with your raises, promotions and capital appreciation from your stocks and home? And growth stories need not worry about cash flow and actual profit. Right?

After all, that’s why you don’t need to worry about such things as ROC. At least that’s what I’ve been told. Because who needs to make back the money that they’ve borrowed or invested, right?

IN CONCLUSION

Maybe I’m just wrong on all of this. That’s what other people are gaslighting telling me to think.

Here’s an example of such wisdom.

Or how about this charming piece?

And let's not forget this classic copout by frameshifting things to the future in order to avoid responsibility for past behavior.

It isn’t that that’s not a factually true statement. The problem is the implicit, subtextual sentimental insinuation of it. I’ve seen and heard this sort of rhetorical debate tactic too many times to count. It’s a dismissive tactic meant to nullify any culpability of past performance and is thought terminating in its purpose. It’s asking for a clean slate to a checkered past.

Are there serious reasons to think that the future will be different than the past? Are there reasons to think that those trait characteristics displayed by people in the past aren’t a patternable phenomenon and are instead a one off? Where’s the proof? And wouldn’t any proof of change exist in the past and thus not be relevant? And that’s the point, to never be held accountable.

People like to speak to the future, detached from the past. What better breeding ground for pathology and fantasy to live out its dream of cope and fallacy.

So, if you actually believe in the rhetorical smokescreen that’s meant to obfuscate matters in a plausible and specious fashion then I invite you to take back that girlfriend who cheated on you. Move back in with that roommate who stole from you. After all, the past doesn’t help you understand the future and what those people will do and by extension what you’re supposed to do. You see how stupid that sounds? I sure hope so.

Let me tell you what really frustrates me in regard to these sorts of tweets. They had many more characters available in their Tweet to generate nuance and context, yet they chose not to.

The reason they didn’t add context is because that was beside the point. The point was to use a specious statement to dismiss and undermine the topic I was discussing without having to provide any evidence on their part. And in some insidious way they think that they’re right by default of my statement being allegedly invalid. FYI, an idea is right based upon its merits not the lack of merit of another idea. So even if I was wrong that doesn’t mean they’re right. But humans can’t be bothered with that.

They weren’t concerned with the truth; they were concerned with confirming their biases.

And guess what? It's that very degree of intellectual lethargy and lack of nuance and contextualization that’s at the heart of today's entire piece. I’ve said it before and I’ll say it again, pathology and bias know no bounds. If you display it outside of the investing realm there’s no reason to think that it won’t creep into your investing decisions. And that’s worth thinking about in and of itself.

So now I’ll leave you to think about such matters.