Red Cat Holdings: RCAT

Ramblings from a weak hand

If I catch myself looking at a stock price too much then I know that there’s something wrong. It doesn’t have to be something wrong with the stock or the company, but with the relationship. This forces me to reevaluate what’s going on. This is all to say that I lack the courage of my conviction to hold onto RCAT. Which kind of sucks. I also suspect that it isn’t RCAT per se but the fact that I’ve taken on more “risk” lately. And RCAT is seemingly the final straw on the back of this investor.

To be frank, it kind of sucks. Their future could seemingly be bright. However, I didn’t get in at a good cost basis. If I had bought when I should have bought ($2-$3 per share when all the news was developing) I’d be more than happy to hold.

It’s also forming the right shoulder on a H&S pattern and I find that to be too much on my already less than idea cost basis.

I don’t like multi-month H&S patterns. Most recently, I saw this predictably play out for ELF.

A 19-month H&S pattern is more concerning than a 3-month H&S pattern, though. I also don’t see any reason for RCAT to break the neckline unless something goes terribly awry with their execution or a market-wide sell off occurs.

Sitting with this itching feeling to sell, I thought that I should revisit this article (which had yet to be published up until this point). The uncertainty and lack of conviction was clear in my writing. As such, I sold.

However, I thought that I could still share this article with you to stimulate your thoughts and to show my thinking around this name.

I MISSED THE MOVE

I’ve been paying attention on and off to the drone space for some time but if it wasn’t one thing it was something else. The sector for years could get any momentum. As such, I failed to stay up to date. I wanted to invest in a commercial or recreational consumer type drone company. What I didn’t want to invest in was a military drone company. Well, you can’t always get what you want. As the saying goes, “take it or leave it.”

Which leads me to the topic of today: RCAT (Red Cat Holdings).

In order to familiarize ourselves with them, let's do a brief overview of their development over the years.

This company had pivoted towards the drone space back in 2016.

I should clarify that they make these types of drones:

Not this type of drone:

Beginning in January 2020 they started bolting on acquisitions to expand their scope.

Upon the Teal acquisition in August 2021, they split their business into two segments – the defense/commercial division and the consumer division.

In March 2023 they signed an agreement to divest their consumer segment to focus on their defense and commercial division.

It took until February 2024 for them to close that sale.

The purchaser of their consumer segment was Unusual Machines. You might have heard of Unusual Machines due to its recent parabolic move as a consequence of Donald Trump Jr. joining its advisory board and people pumping it.

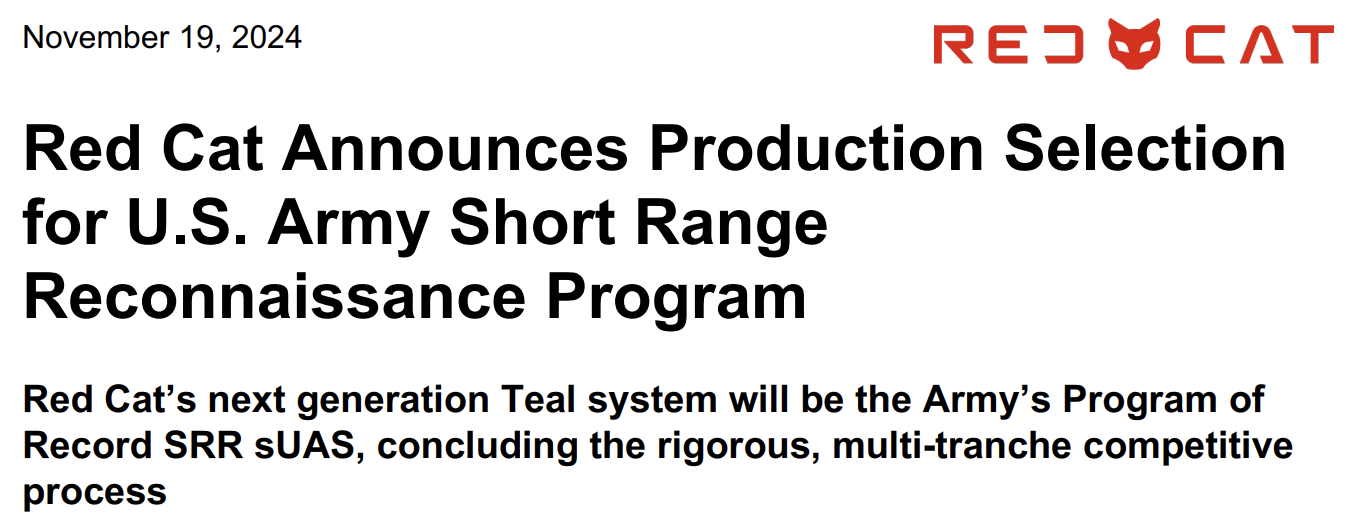

In December 2023, RCAT released a press release noting how they were selected by the DoD as one of two finalists in the SRR (Short Range Reconnaissance) program.

Interestingly enough, the early part of December 2023 was an incredibly volatile time for the company.

Their stock fell 40% on a $9.2M public offering (on a market cap of $42M). Then on the 12th they released their earnings. Some good news came on the 14th when they revealed that they were a finalist for the SRR program, in which their stock spiked nearly 30% to lose most of those gains by the end of day.

I tried looking up the cash tag $RCAT on Twitter for that time period but was mostly inundated with something called Rocket Cat.

The investing case for Rocket Cat was pretty solid.

Once you knew about Rocket Cat:

You would buy Rocket Cat:

Which lead to this happening:

Which ultimately resulted in this:

But I digress. However, I did want to do thorough due diligence. For instance, I don’t recall the Kerrisdale research report mentioning Rocket Cat.

But back to our similar yet different colored aeronautical cat: RCAT.

Had you bought on Dec 14, 2023, when the news of them being a finalist occurred, you’d been up 2,300% a couple of weeks ago and 1,300% currently. But as I noted in one of my last articles, those things practically never happen.

Alright, this now brings us into 2024. If we fast forward to November, we’ll discover that RCAT does indeed win the SRR program.

I’d like to say that although it took me less than 500 words to cover their Batman origin story, they had to slog through a lot.

Yet again, it’s not like this program started a few months ago and quickly came to a close.

This is from their Q1 2022 (September 2022 since they don’t follow a normal Calendar year) Conference Call:

“Teal drones are made in the USA and with the ban on drones and even drone components made in China coming into effect, this is another competitive advantage for Red Cat. Additionally, we continue to move forward with the DoD in the Short-Range Reconnaissance, SRR program. And we are participating in the second tranche of that program.”

From January 2020 until the last few months the stock performed terribly. Or, in line with its underlying performance. It all depends on how you want to look at it. Either way, it underperformed the S&P 500.

For 4 ½ of the last 5 years, RCAT had a 0% CAGR. Well, that has turned into a 50% CAGR all because of the last 5 months of stock movement.

This so-called overnight success has been 9 years in the making. Even if you want to start the clock from their Teal acquisition, it was still 3 years in the making. And don’t get too far ahead of yourself, no sales have happened yet, insofar as the SRR program is concerned. It took 3 years just to get to a point where they’re in a position to produce and sell. There’s still plenty of opportunities to mess this up.

Had you bought RCAT on that Q1 2022 press release, you would have ultimately suffered an 80% drawdown for over 2 years. Interestingly enough, your thesis would have played out and you would have outperformed the S&P 500, ultimately up to this point.

To sum things up.

2021: They bought something that would let them get their foot in the door.

2024: They finally got their foot in the door.

2025: To be seen

Had the whole Ukraine/Russia conflict not acted as a catalyst for drone warfare, who knows where this company would be.

I see a lot of commentary around the Chinese drone banning but that’s been going on for years. Even with all the alleged bans in place, right now, you can still buy a DJI (Chinese) drone.

According to this article:

DJI has faced strict U.S. government regulation in recent years. In 2019, Congress “banned the Pentagon from buying or using drones and components manufactured in China.” In 2021, the Department of Defense added DJI to the list of “Entities Identified as Chinese Military Companies Operating in the United States.” Multiple states, including Arkansas, Florida, Mississippi, and Tennessee, have banned DJI drones from government use. In 2024, DJI accused U.S. Customs and Border Protection of blocking imports, reportedly under the Uyghur Forced Labor Prevention Act, a law that prohibits products made with forced labor from China. This has not publicly been confirmed.

The most significant U.S. action against DJI in 2024 came from Congress. Last September, following arguments that DJI was a threat to national security, the U.S. House of Representatives passed the Countering CCP Drones Act with bipartisan support. If signed into law, the bill would add DJI to the Federal Communications Commission’s Covered List, effectively banning new DJI drones. The act holds bipartisan support in the Senate.

One of the takeaways from all of this is that there’s been a lot of hoopla over the last 5 years and it seems to take a long time for things to pan out and add up.

VALUATION:

The stock has the entire SRR contract priced into it.

Long story short, there’s a lot of back and forth about how much the contract is worth in totality and what it is per drone. What I can say is that it’s for 5,880 systems. Each system has 2 drones. There’s back and forth about whether it’s $45,000 or $65,000 a drone. Best case scenario is the program is worth $764.4M and worst case it’s worth $529.2M. Either way, it’s all priced into the stock. Then of course, there’s others saying that it's worth not much more than $300M in the next 5 years.

The point of the above paragraph isn’t to display my ignorance but to demonstrate that even the most ignorantly optimistic forecast in regards to the SRR program is priced in.

On the Q2 conference call they guided revenue in the range of $80M- $120M. Meaning that RCAT is trading at a FWD EV/S range from 5.7x to 8.5x.

You could also make the argument that Anduril (private company) is trading at mid to high teen EV/S multiples and that RCAT should to. As such, it could go higher due to multiple expansion. Which is a funny thing to say because normally the opposite is the case. I said it’s an argument, not that it’s a good argument. Because you could also make the argument that Anduril is coming to eat RCAT’s lunch. For instance, RCAT has a 25,000 sq ft. facility and Anduril is building a 1.5M sq ft. facility.

The best I can tell is it’s something like this: It’s proof of concept and a viable business model that’s demonstrated that they can indeed get bigger contracts with major players (DoD). And then the subsequent implications that go along with that. Coupled with anticipation of Western Nations wanting to stockpile drone systems and or more active war zones utilizing them in the near future.

The SSR contract is a symbolic representation of what is to come. Think of their efforts over the last few years as them studying and the SRR win as them finally passing the LSAT.

It’s a big win and indication of attainable possibilities to come. Them being and still being a small cap company means that they don’t need giant contracts to meaningfully impact their earnings. Which is good because so far there doesn’t seem to be a ton of money pursuing this industry, although the expected belief is for that to change.

The premium applied to the stock was in part people getting overly ecstatic but it’s also due to the anticipation of this contract helping improve their pathetic bottom line. If they have any hope of being cash flow positive, they need to ramp production to improve their margins.

The analysts' projections I’ve seen were estimating fair value of $7-$9 if they were to get the SRR contract. Well, the stock is sitting in the middle of that range (as of editing this, it’s above $9). Normally, I don’t rely or reference other people's forecasts but it’s now in the past, the moves already been made, I don’t care to do my own modeling and the modeling's I’ve seen look accurate enough.

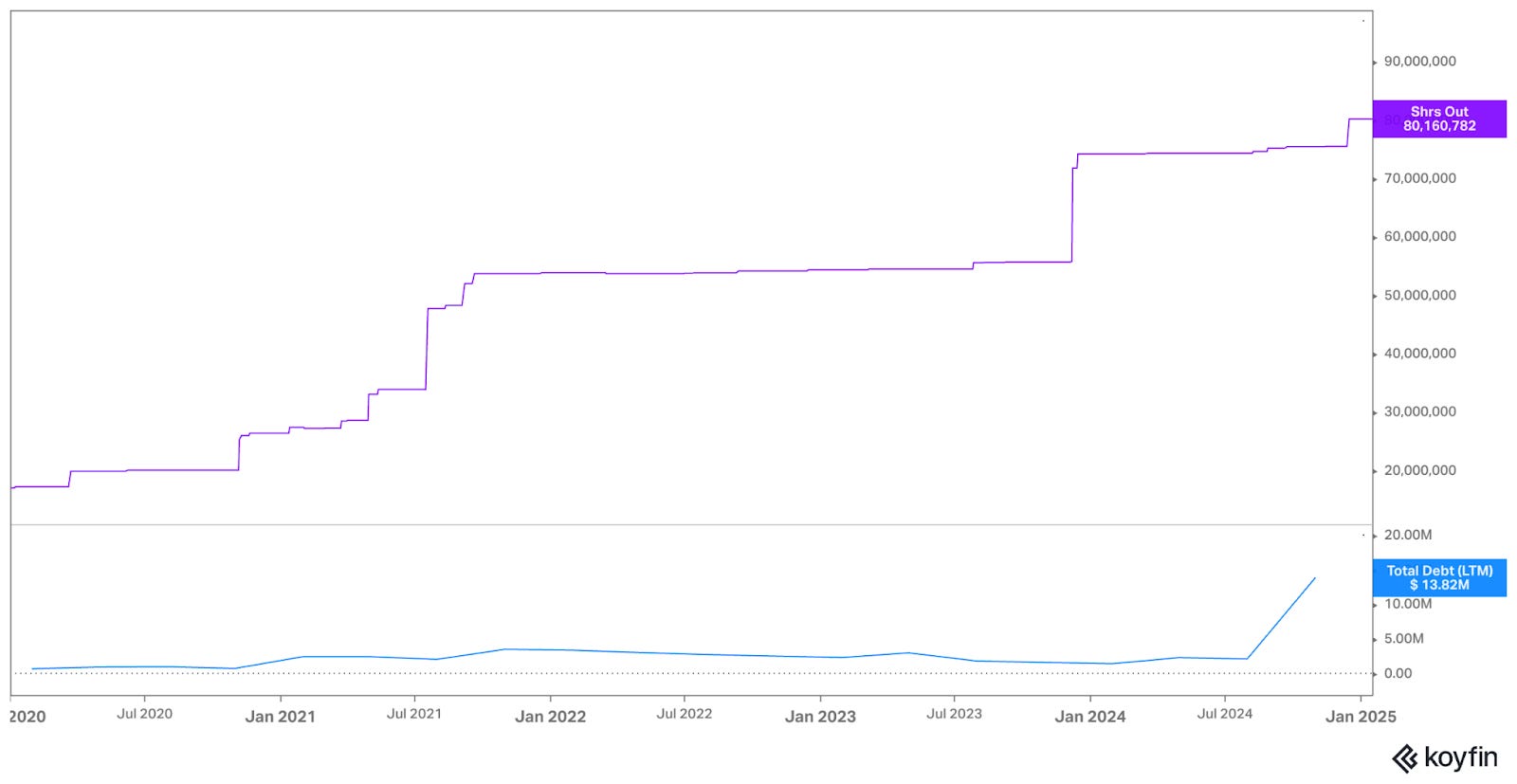

A reasonable question might be, how has a profitless, cash burning enterprise managed to stay afloat for the last several years? If your answer was diluting shareholders then you’d be correct. Impressively, they’re not burdened with much debt. Matter of fact, they have suspiciously low debt (for now). Which is good for anyone looking to enter into a position since we’ve gotten to sit out the dilution thus far.

And I do mean thus far.

They’re locked, loaded and ready to issue according to their November 14, 2024 S-3 Filing.

Jeff Thompson had this to say about cash, cash flows and dilution.

“Right, yeah. He just emailed me a bunch of the ones from some of the analysts on there. But let me just also just kind of round up because a lot of the -- I bet you all the questions are going to be coming in are about fundraising. So, as Leah just said, we've got cash in the bank [way into] (ph) the quarter. We just closed on $6 million worth of, we got some more cash. We got about possibly $3 million coming in January from the new features on the army. We believe that the debt holders have warrants that are not cashless, that are weighing the money. We expect them now that their shares are registered to probably exercise those. That's another $5 million. So, we are very healthy to wait till we need to make a decision to hopefully raise as little money as possible. As we also have been notified to that we should be applying for the Office of Strategic Capital, which does loans between $10 million and $150 million. They just appropriated $998 million for that program. It's available now. We're applying for it in early January. We're supposed to know by the end of February, early March, if we can receive that $10 million to $150 million. They only want to give it to 10 or 15 companies. There's about 15 categories. I think we check off six or eight of them. We're a perfect candidate. We have a program of record. So, we hope that we can get that Strategic Capital, a very low interest. And there's also, you can read it. It's all out there publicly that you can also waive repaying the loan for years. So, it's very grant-like type of funds. So, we've got plenty of ways to access capital without dilution.”

Then of course there’s the curse of short seller discussions among the retail investor base. You know there’s a good chance that you have a bunch of garbage minded investors when the mention of short interest is a common point of conversation.

Also, their newest presentation is a year old!

I don’t want to go so far as to say that RCAT is a long shot but I would say that there’s abnormally high risk with this name relative to what I normally invest in, especially at this price point.

RANDOM RAMBLING

Simply put, a threat to this stock is that it fills the gap from its SRR announcement. This would imply a 42% downside. Therefore, the reward should be at least commensurate with that risk. Which raises the question, what will make this stock go up 42%?

I don’t know.

It’s not like the SRR program isn’t fully baked in. On the other hand, as I’ve already noted, something would have to go terribly awry for it to fill the gap. At that point, it would be interesting to look at again but I suspect that the fundamental story would also have to somehow be impaired, thus making it not an attractive opportunity.

I’m also dissuaded due to my belief that there are good enough odds that the Russia/Ukraine conflict will deescalate or at least not further escalate. On such headline news, I can’t imagine RCAT not taking a big hit.

The bull case of a few months ago is different than today. Back then it was one of assessing the odds of an SRR program win.

The bull case as of now seems to be one that their SRR win is setting a precedent that will enable them to continue winning future contracts with minimum concern of execution risk and obsolescence risk (which doesn’t seem unreasonable).

I’m quite torn. Normally I write either bearish articles or bullish articles. This article is an I don’t know and I could reasonably see either outcome article. If I had to, I’m leaning towards bearishness, at least in the short term (upon updating this article, I’m surprised that I said this).

Normally when I read a short report, I get an intuitive sense of whether it’s stupid or not. When it comes to the recent Kerrisdale report, I feel that some of their concerns aren’t negligible. For instance, their brainchild (George Matus) leaving and their numerous overdue promises not materializing puts me on guard. Sure, that’s now in the past but still…

We can’t ignore thesis creep. Matus was a large part of the bull thesis. Now, you could say that they’re reaping the fruit from him but what about the future? Who’s going to be the cutting-edge innovator now?

And comments like this from the CEO during theTown Hall meeting don’t make me feel any better.

“Well, the R&D budget is not going to go crazy just because we won SRR. So, I'm coming down on the Scrooge side of that, we've done basically five years of R&D.”

On one hand you can say that they need to focus on the task at hand and proving themselves. And fair enough. But on the other hand, this is a nascent industry. Letting your guard down and not being forward-looking can hurt you in a hurry.

However, their recent acquisition of Flightwave with the accompanying Edge 130 drone demonstrates that they could maintain their strategy of M&A. As such, they can just acquire other brainchildren. It’s a strategy of buying other people's R&D via M&A rather than technically spending on R&D to get the same result. It also helps consolidate the industry. It also demonstrates it’s a viable strategy for growing their services since the Edge 130 is a MRR (medium range reconnaissance) drone.

Since this is a preliminary assessment of matters that I’m sharing with you today, I don’t have a lot of answers to my questions. For instance, what happened to Droneshield?

To see that a stock can do this makes me wonder if RCAT will do this.

So far Droneshield has fallen 74% from peak. I started this section by saying that it could reasonably fall 42% (yet again, I didn’t realize I was so bearish sounding). This is a very abstract overlay between two loosely tangentially associated companies within a broader industry. I merely place this chart here to demonstrate that these story stocks, with inflecting fundamentals, can get ahead of themselves and that market structures and participants can just as easily undershoot a stock after overshooting a stock.

There also seems to be a lot of mention of EOS while researching Droneshield.

I know I’m getting off on a tangent but my point is that there’s a lot of these small cap drone industry names. The reason I bring up these ASX listed small cap drone defense companies is because there’s multiple angles to play this drone theme. A similarity that many of them share is that they all found a bottom around the time of the Russian invasion of Ukraine. A serious question I have is if they will all find temporary or even multi-year tops upon news of a ceasefire?

Insofar as the drone industry is concerned, there’s all types of drones. Although today's piece is dedicated to reconnaissance/multirotor drones…sUAS (small Unmanned aerial system).

It seems that drones are becoming as much of a software play as they are a hardware play. All of this makes me wonder if they’re a one and done or a flash in the pan.

It’s bad enough that there’s immense competition between the drone manufacturers themselves but now we have to layer on this game of cat and mouse between them and the counter drone systems being developed. Their relevance is contingent on continuing satisfactory performance above status quo in regards to competition but also towards the opposition (c-sUAS counter small Unmanned Aerial system).

As you can tell, I’m curious yet uncertain of much. I’ve written this piece in hopes of ironing out some of that uncertainty. It has not. When these kinds of things happen, I’ve either missed the move or it’s still too early. Normally, I land in the still too early category. But how can it be too early, I’ve missed the move in these names by two years?

Much of this uncertainty is the consequence of cost basis. Had I invested in the $1 or $2 range this article wouldn’t exist. I’d be fine with such uncertainty due to the margin of safety I would have built in. Which is to say that this article is an attempt to assuage my insecurities about the delta between price, value and future value which will get created or destroyed.

I’ve bought shares of RCAT. However, I’m a weak hand and if it falls beyond a certain point I’ll be selling. The problem with such stop losses is that if it falls below my designated point, it will probably have punched through and thus doubled the losses that I was trying to prevent.

Update: I sold this with a gain. Seemingly, I needed these thoughts to incubate in the back of my mind for a couple of weeks before I pulled the plug. Looking back on this I can see how I’ve been unsettled in holding shares. I was much less bulled up than I thought. And that is the pleasant benefit of writing your thoughts down, our memories can play tricks on us.