Carvana Case Study

The Stakes Aren't Just Paper Profits — We're Talking About an Actual Porsche, Albeit Used.

Ultimately, I’m under the belief that you shouldn’t bicker over a few percentage points when it comes to entering a position into an investment. However, with that said, I’m well aware of the outsized difference it makes in regards to your returns.

Let’s take $CVNA as an example.

Had you bought $CVNA for its close price of $3.83 on Dec 28, 2022 you’d be up 4,525%.

However, if you waited until Dec 29, 2022 to buy at the close at $4.45, you’d be up 3,881%.

Meaning that if you bought $0.62 higher or 16% higher it cost you 644% in total returns.

HAD YOU JUST BOUGHT & HELD AMAZON

Of course, to a large extent, this doesn’t matter. Which is why casual comments like, “let your winners run” leaves a lot undiscussed.

Why?

Because the probability of you holding onto $CVNA this entire time is practically zero. And by this entire time, I mean since Dec 28,2022. Which is why discussions around Amazon aren’t necessary to convey this point.

Carvana has had in the last two years:

Two 50% drawdowns

Three 20% drawdowns

Is on its third 30% drawdown

You come to realize that the shareholder base has turned over numerous times over $CNVA 4,500% run-up.

This is why people who say, “had you bought Amazon back in …. You’d be up ….%. That’s all fine and dandy, except no one still owns it from back then for similar reasons.

It reminds me of the Lassonde curve.

The same people playing the exploration mining companies sell out on good news. Then a new set of buyers come in due to the trade being de-risked. The old players sell out because they’ve gotten the cream off the crop. Other people sell out because the trade becomes less exciting and it’s, “never wrong to take profits”, or, “don’t be greedy”.

It’s similar to distressed investors. Many of them play that part of the cycle. They’re in it for a good time but often not for a long time. There’s nothing inherently wrong with this. But what it goes to show is that you have numerous cohorts with varying styles which minimizes the probability that any one individual will have captured Carvana's total gains.

Pertaining to $CVNA, some people bought it on mere speculation, others bought it in anticipation of a rebound due to it being the end of tax loss selling. Others might have purchased it for fundamental reasons but did their fundamental analysis also probably say that the stock was only worth a few hundred percent more, at best? Which means they sold out due to it reaching fair value. Then at some point you had momentum traders jump on the bandwagon. Then as fundamentals started improving or stopped worsening a new set of fundamental investors came into the picture. So on and so on. The churn of shareholders has probably been replaced numerous times since then. Meaning, that no one has capitalized on the majority of the gains which could have theoretically been had.

What percentage of shareholders do you think sold out here?

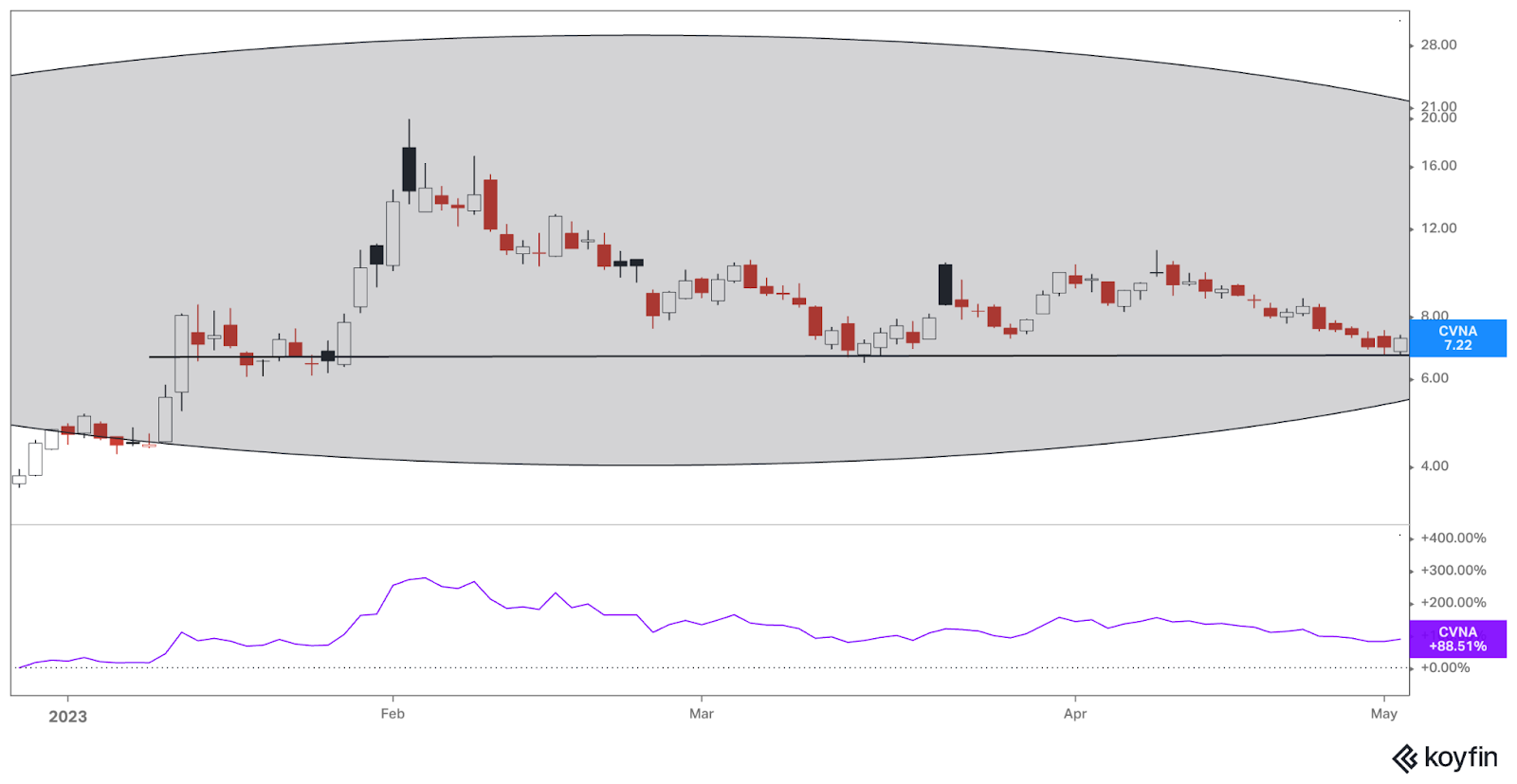

Sure, that looks innocent enough, but let's zoom in.

That might be considered a wonky head & shoulders, lower high, descending pennant. It doesn’t matter if it is or not because people don’t need to be informed to make decisions.

And let’s not forget the poor sentiment in the atmosphere due to many people having a terrible 2022, with the overall stock market being down and inflation roaring its ugly head. That recency/anchoring bias is hard to overcome.

That zoomed in chart only goes to May 2, 2023. For 4 months of holding, you managed to be up 88%. Add on the fact that it’s testing a support line and it has earnings coming out on May 9, 2023 and I assure you that a lot of people were telling themselves

“That it might be wise to take their profits and run.”

“No need to risk it.”

“It’s their fiduciary responsibility to lock in profits.”

Oh, and let’s not forget, that by May 2, 2023 they would have gone from being up 277% down to “only” being up 88% due to a 3-month long drawdown/consolidation.

Just in this one snapshot, the number of players shaken out was probably incredible.

Oh, and what happened on the May 9 earnings report…

Yeah, it gapped up 24% and a whole new set of people chased.

DOLLARS & PERCENTS

Percentages and how they translate with dollar figures can play a lot of mind games too.

As I noted in the last section, although they were still up 88% in a matter of months, they were massively down from an ATH of 277%.

A lot of mind games go on in these situations and that’s how people can get shaken out of trades. People get anchored to their ATH percentage gains. And in a drawdown, this is how selling can beget more selling. And that’s before factoring in volume shelves and recent entrances cost basis.

Take for instance their current drawdown.

Carvana peaked out on November 25, 2024. Had you bought that day, you would have lost 32% of your money.

However, if you were this phantom person who’s bought and held since December 28, 2022 you would be looking at your stock portfolio to see that your gains went from 6,709% to 4,525%. Put yourself in their shoes (theory of mind exercise). They would have lost 2,184%!!!

Let’s put this in simple dollar terms, since that’s how a lot of unserious people think about their stocks, rather than in percentage terms.

Let’s say some retail investor invested $1,000 into Carvana on December 28, 2022. They would have gone from $68,090 to $46,250. Which is to say that over the last 1 ½ months they’ve lost $21,840.

Which is to say, that they lost the ability to purchase any of these cars.

As the returns start adding up in nominal dollar terms the more “real” those returns become and the more people want to protect them because they translate to real purchasing power.

All of this is to illustrate the following:

1. The Importance of Timing:

Small differences in entry points can lead to significantly different outcomes in investment returns.

2. Volatility and Investor Behavior:

The volatility of stocks like Carvana can lead to frequent changes in the shareholder base. Many investors sell during drawdowns & price rises, which contributes to the churn of ownership and diminishes the likelihood of any single investor capturing the full gains.

3. Psychological Factors in Investing:

Investors are often influenced by psychological biases which often lead to premature selling and missing out on potential gains.

4. The Nature of Investment Holders:

Long-term holding is often unrealistic for many investors, especially in volatile markets. The passage suggests that even if a stock has substantial gains, the number of investors who actually hold onto it throughout its ups and downs is minimal.

6. Market Dynamics:

The discussion emphasizes the cyclical nature of market participation, where different cohorts of investors enter and exit based on varying motivations—speculation, fundamental beliefs, or reaction to market news.

7. The Importance of Perspective:

The exercise of putting oneself in the shoes of other investors can provide insights into collective behavior and decision-making processes, which can be beneficial for understanding market movements and your involvement come that day.